STATE OF THE ECONOMY: 1)Bank of Canada – Release of the Financial Stability Report; 2) Gross domestic product by industry, March 2026

1)Bank of Canada – Release of the Financial Stability Report

May 28, 2026

Opening statement

Good morning. Deputy Governor Toni Gravelle and I are pleased to be here to discuss the Bank of Canada’s Financial Stability Report, or FSR.

A stable and efficient financial system is essential to our economy. It supports growth and helps households and businesses to save, invest and manage risks. We monitor the financial system closely—and each year, we publish this report to share our assessment with Canadians.

The FSR is very different from our Monetary Policy Report. It is not a forecast, and it does not guide interest rate decisions. Instead, it gauges the resilience of the Canadian financial system and explores the key risks and vulnerabilities that could undermine that resilience.

I’ll start today with our overall assessment, then highlight a few key areas we are keeping a close eye on. Deputy Governor Gravelle will then delve into the conditions across financial markets, households, businesses, banks and non-bank financial intermediaries.

Overall, Canada’s financial system has functioned well through a challenging year. Households and businesses remain in stable financial condition, and banks have strengthened their capacity to absorb shocks.

However, vulnerabilities have increased in some parts of the system. Stock and corporate debt valuations have risen and are high relative to historical norms. This makes markets more vulnerable to a sharp correction.

The issuance of global sovereign debt is also rising, and hedge funds are playing a bigger role in buying that debt, often using borrowed money. In normal times, hedge fund activity helps keep markets running smoothly. But if conditions become strained, this activity could amplify stress and disrupt core funding markets.

Individually, these and other vulnerabilities look manageable. However, the economic and geopolitical environment has become more volatile. And this has made it more likely that a new shock or a combination of shocks could cause several vulnerabilities to crystalize at once. If this were to happen, these vulnerabilities could interact and reinforce each other.

A cascading series of events could cause a sharp loss of investor confidence and lead to a spike in demand for liquidity or rapid asset sales. Funding markets could come under pressure, and stress could spread more broadly.

To be clear, the FSR is not about what we expect will happen. It is an assessment of how existing vulnerabilities—or pockets of stress—could amplify shocks and ultimately spread across the financial system.

At the time of the 2025 Report, we were concerned that tariffs and trade uncertainty could lead to market volatility, strains on liquidity or even market dysfunction.

So far, the impacts have been less widespread than we originally feared. But this risk has not gone away, and the future of Canada’s trade relationship with the United States remains uncertain.

More recently, the war in the Middle East has added to global uncertainty, leading to volatility in some markets and short periods of reduced liquidity. Even with these pressures, markets have continued to function well.

But it remains unclear how long the war will last or how it might be resolved.

New risks are also emerging, particularly from artificial intelligence. AI is expected to boost productivity and economic growth over time, but it is sparking concerns about disruption in some sectors and about overinvestment. AI may also increase the speed, scale and sophistication of cyber attacks.

Now let me turn to Deputy Governor Gravelle to talk about conditions in the five sectors we monitor.

Thank you, Senior Deputy Governor.

I will start with households, where the overall picture is similar to last year.

Canadians continue to carry high levels of debt relative to their income, but overall household wealth has risen. And the share of borrowers who are behind on debt payments has stabilized.

In recent years, we’ve highlighted the risk of payment shocks when households renew pandemic-era mortgages. To date, most borrowers have managed this risk well. With the final wave of these renewals set to happen over the next 12 months, we expect this risk to have fully passed by the second half of 2027.

I’d like to stress that this overall picture masks important differences. Some households face far greater strain than others, and those with the highest debt burden have very little financial flexibility to cope with a job loss or an unexpected expense.

Business financial health is broadly stable—even in sectors most exposed to shifting US trade policy. But a downturn could put pressure on margins and make borrowing more difficult.

The main concern for both households and businesses is a geopolitical or economic shock that leads to a deep recession and a sharp rise in unemployment.

Canada’s large banks have become more resilient over the past year, with higher profitability and healthy capital buffers. They have also set aside additional funds to absorb potential loan losses. This positions them to support the economy and financial system, even in a severe downturn.

Vulnerabilities related to non-bank financial intermediaries continue to grow. Hedge funds are taking on more leverage, in part to finance their purchases of government bonds. This supports market liquidity but can also be a source of fragility.

I’ll end with financial markets. Recent geopolitical events have led to bouts of volatility, but financial markets have generally proven resilient.

To summarize, our overall view is that the Canadian financial system remains well positioned to weather shocks. Over the past year, it has faced repeated tests. While there have been some strains, those episodes did not lead to broad-based financial stress.

Still, we must stay vigilant. We will continue to monitor vulnerabilities closely and remain in regular contact with financial system participants and with domestic and international partners.

A stable and resilient financial system absorbs shocks rather than amplifying them, and that benefits every Canadian.

With that, the Senior Deputy Governor and I are happy to take your questions.

Content Type(s): Press, Speeches and appearances, Opening statements

Subject(s): Financial system, Financial markets, Financial stability

2)Gross domestic product by industry, March 2026

Courtesy: Stats Can: Released: 2026-05-29 by Stats Can, https://www150.statcan.gc.ca/n1/daily-quotidien/260529/dq260529b-eng.htm

Real GDP by industry

March 2026

-0.1%

(monthly change)

Source(s): Table 36-10-0434-01.

Real gross domestic product (GDP) edged down 0.1% in March, partially offsetting February’s increase (+0.2%) and driven by contractions in goods-producing industries.

Chart 1

Real gross domestic product edges down in March

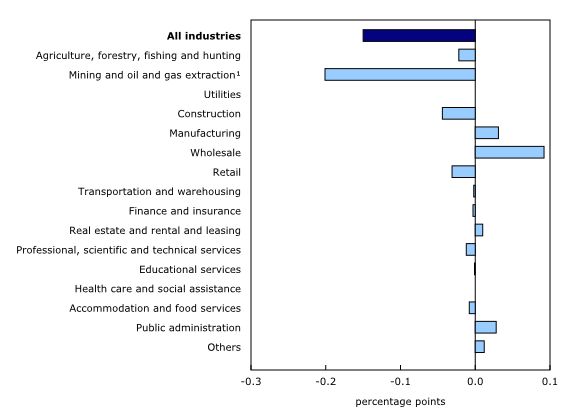

Goods-producing industries contracted 0.8% in March, more than offsetting February’s expansion. This was the fifth decline in the last six months. The decrease in March was in large part a reflection of lower activity in the mining, quarrying, and oil and gas extraction sector and in the construction sector. Services-producing industries tempered the decline, edging up 0.1% in March, led by an increase in wholesale trade. Overall, 8 of the 20 industrial sectors contracted in March.

Mining, quarrying, and oil and gas extraction contracts in March

Mining, quarrying, and oil and gas extraction decreased 2.1% in March, driven by contractions in most comprising subsectors.

Chart 2

Mining, quarrying, and oil and gas extraction sector contracts in March

Oil and gas extraction decreased 2.0% in March on a broad-based decline across industries. Oil and gas extraction (except oil sands) was down 2.3%, the largest drop in over a year, as lower crude petroleum extraction in the Western provinces and Atlantic Canada contributed to the decline. Lower natural gas extraction further contributed to the decrease in March.

Oil sands extraction was down 1.6% in March, reflecting lower synthetic crude production in Alberta. This was the third decrease in oil sands extraction in four months. Several factors weighed on the overall output in March, including longer than anticipated maintenance and repairs at some upgrading facilities, natural gas supply disruptions to these facilities, along with inclement weather across the Prairies. Pipeline transportation contracted 1.2% in March, down for the fourth month in a row. Lower pipeline transportation of natural gas (-2.8%) led the decline due to lower deliveries to the oil extraction facilities in northern Alberta and lower overall natural gas distribution (-2.2%). Crude oil and other pipeline transportation rose 0.4% in March.

Mining and quarrying (except oil and gas) decreased 3.9% in March on widespread contractions across all comprising industry groups. Coal mining (-13.9%) led the decline, as extraction of coal dropped in Alberta and British Columbia, coinciding with lower train carloadings and exports of the product.

Metal ore mining (-3.0%) contracted for the fourth consecutive month in March, driven by decreased copper, nickel, lead and zinc ore mining (-9.5%), coinciding with lower exports of copper ores and concentrates in the month. Decreased activity in gold and silver ore mining (-1.9%) further contributed to the decline, coinciding with falling gold market prices in March.

Construction down for the second month in a row

The construction sector decreased 0.6% in March on weaknesses in most comprising subsectors, following a sharp decline in February (-1.5%).

Engineering and other construction activities (-0.9%) and residential building construction activity (-0.8%) contributed the most to the decline in the construction sector in March. Construction activity in most residential building types fell in the month, with alteration and improvement activities and construction of single occupancy and apartment-type buildings contributing the most to the decline.

Retail trade down in March

The retail trade sector contracted 0.6% in March, partially offsetting the back-to-back monthly expansions in January and February.

General merchandise retailers (-2.7%) contributed the most to the decline in the sector in March, the first contraction in six months. Retailing activity at building material and garden equipment and supplies dealers (-3.0%) was another large contributor to the decline. Gasoline stations and fuel vendors (-1.9%) further added to the decline in the retail trade sector, coinciding with a jump in gas prices, arising from the supply shock caused by the conflict in the Persian Gulf.

Wholesale trade up on the largest back-to-back monthly growth rates in over four years

Following a 1.4% expansion in February, the wholesale trade sector rose 1.8% in March as most activities expanded in the month. This marked the sector’s largest single-month growth since May 2023.

Chart 3

Wholesale trade grows in March

Increased wholesaling activity in machinery, equipment and supplies (+6.4%) led the growth in March, coinciding with new product releases and deliveries to government clients.

Public sector rises in March

The public sector aggregate (comprising educational services, health care and social assistance, and public administration) edged up 0.1% in March, driven by an increase in public administration.

Following back-to-back monthly declines, public administration increased 0.4% in March, led by expansion in local, municipal and regional public administration (+0.6%) and provincial and territorial public administration (+0.5%). The federal government public administration was essentially unchanged in the month, as a decrease in public administration (except defence) (-0.3%) was offset by higher activity in defence services (+1.0%).

Arts, entertainment and recreation grows following Olympic break while special events viewership contracts

Performing arts, spectator sports and related industries, and heritage institutions rose 6.9% in March, led by a rebound in spectator sports as the National Hockey League (NHL) resumed its regular schedule following the suspension of play in February to allow some of its players to compete for their countries in the Olympic games.

At the same time, information and cultural industries contracted 0.2% in March. Lower activity in the month at radio and television broadcasting stations (-13.4%) followed a spike in February, which coincided with the airing of the 2026 Winter Olympics.

Chart 4

Main industrial sectors’ contribution to the percent change in gross domestic product in March

Advance estimate for real gross domestic product by industry for April 2026

Advance information indicates that real GDP increased 0.4% in April. Increases in mining, quarrying, and oil and gas extraction, manufacturing and transportation and warehousing were partially offset by decreases in agriculture, forestry, fishing and hunting. Owing to its preliminary nature, this estimate will be updated on June 30, 2026, with the release of the official GDP by industry data for April.

First quarter of 2026

GDP by industry edged up 0.1% in the first quarter of 2026, as increases in services-producing industries (+0.3%) more than offset declines in goods-producing industries (-0.4%). This follows a decline of 0.1% in the fourth quarter of 2025.

Transportation and warehousing (+1.2%) was one of the largest positive contributors to the quarterly increase in the first quarter of 2026. This was the largest quarterly increase in transportation and warehousing since the third quarter of 2023. Most subsectors posted increases in the first quarter of 2026, with postal service, couriers and messengers (+7.3%) contributing the most to the expansion, as postal service (+16.2%) rebounded from the Canada Post strike that occurred at the end of 2025.

Information and cultural industries rose 1.6% in the first quarter of 2026, driven up by computing infrastructure providers, data processing, web hosting, and related services (+4.4%), its second consecutive quarterly expansion. Software publishers (+2.5%) further contributed to the sector’s growth.

Retail trade rose 1.0% in the first quarter, with health and personal care retailers (+3.5%) and general merchandise stores (+3.2%) contributing the most to the sector’s quarterly growth.

The mining, quarrying and oil and gas extraction sector expanded 0.4% in the first quarter of 2026, offsetting most of the 0.4% contraction in the fourth quarter of 2025. Leading the growth in the first quarter of 2026 was higher oil and gas extraction (except oil sands) in Saskatchewan and off Canada’s Atlantic Coast. An increase in natural gas extraction across the country further added to the growth. Tempering the growth was a 1.5% contraction in oil sands extraction due to longer than anticipated maintenance and repairs at some upgrading facilities in Northern Alberta, along with a frigid start to the year across the Prairies.

The utilities sector increased 1.9% in the first quarter with electric power generation, transmission and distribution (+2.6%) leading the growth. Improving drought conditions in certain parts of the country and the restart of a nuclear generating station in Ontario, following a period of refurbishment, contributed to the increase.

The construction sector (-1.3%) was the largest detractor to growth in the first quarter. Engineering and other construction activities (-4.2%) and residential building construction (-0.4%) both contributed to the decline for a second consecutive quarter. The decline in engineering and other construction activities brought this subsector to its lowest level since the first quarter of 2025, while residential building construction fell to its lowest level since the third quarter of 2024.

Agriculture, forestry, fishing and hunting fell 3.5% in the first quarter of 2026, the sector’s first contraction since the third quarter of 2023. Crop production (-4.7%) was the main driver behind the decrease in the first quarter of 2026, reflecting lower expected yields for the year.

The manufacturing sector edged down 0.3% in the first quarter of 2026, representing its second consecutive quarterly decline and the fourth decline in the last six quarters. Decreases in non-durable goods manufacturing (-0.4%) and durable goods manufacturing (-0.2%) drove the decline in the first quarter. Several major auto assembly plants in Ontario extended their winter shutdowns in the early parts of the quarter, resulting in reduced auto production and contributing to the decline in motor vehicles and parts manufacturing (-5.8%). Petroleum and coal product manufacturing (-3.3%) contributed the most to the decrease in non-durable goods manufacturing, as maintenance work at some refineries resulted in lower production.